.svg)

What Corporate Treasurers Can Learn from USDC’s Transparency Model

June 16, 2026

Stablecoins have become an increasingly important part of digital financial infrastructure. What began as a tool primarily used within cryptocurrency markets is now attracting attention from payment providers, fintech companies, treasury teams, and institutional investors.

As adoption expands, the conversation is changing.

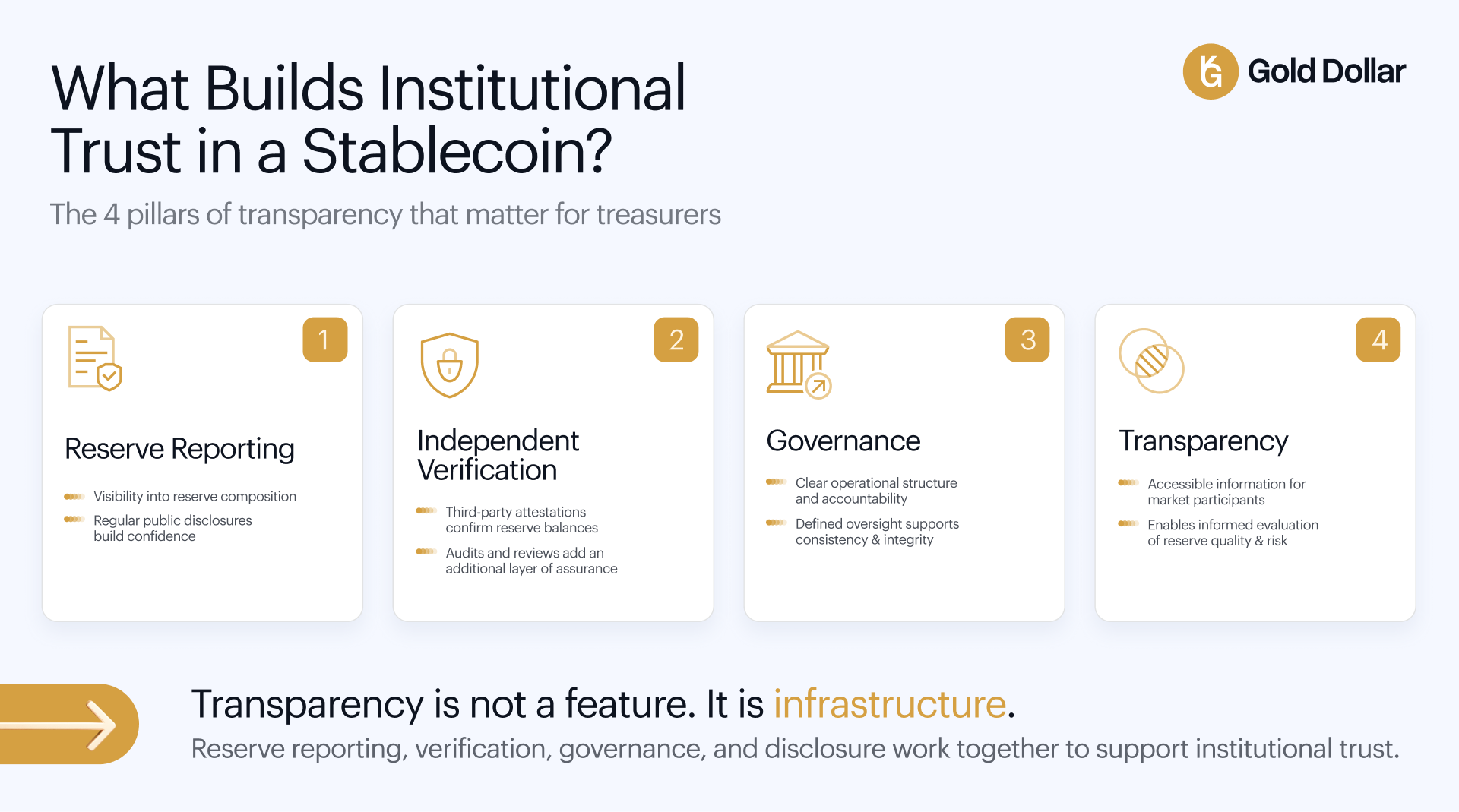

For many organizations, the key question is no longer whether a stablecoin maintains its peg. Instead, greater attention is being placed on reserve transparency, governance, reporting standards, and the mechanisms that allow users to verify how an asset is backed.

Among the largest stablecoins, USDC has become one of the most widely referenced examples of how transparency can support institutional trust.

While different stablecoin models serve different purposes, there are important lessons that corporate treasurers can draw from USDC's approach to reserve reporting and operational transparency.

Why Transparency Matters for Treasury Operations

Corporate treasury teams are responsible for managing liquidity, preserving capital, and ensuring operational continuity.

When evaluating financial instruments, treasury professionals typically look beyond market adoption and focus on questions such as:

- How are reserves managed?

- Who verifies the reserves?

- How frequently is information disclosed?

- What governance structures exist?

- How easily can risk be assessed?

These principles are not unique to digital assets. They have long been standard considerations across banking, money market funds, and traditional treasury management.

As stablecoins become increasingly integrated into payment systems and financial operations, many treasury teams are applying the same evaluation framework to digital assets.

Transparency becomes important because it allows organizations to understand how an asset is structured and whether its reserve model aligns with their risk management requirements.

The USDC Transparency Model

USDC, issued by Circle, has consistently emphasized reserve reporting and disclosure as core elements of its market positioning.

The company publishes regular reserve reports and monthly attestations prepared by independent accounting firms. These reports provide visibility into reserve composition and the assets supporting circulating USDC supply.

This approach has helped establish a level of familiarity among institutions exploring digital asset infrastructure.

Rather than requiring market participants to rely solely on issuer statements, reserve data is communicated through a structured reporting process designed to provide ongoing visibility.

For treasury teams, this creates a framework that is familiar to traditional financial environments where verification and disclosure are expected components of risk management.

Attestations and Independent Verification

One of the most important concepts within stablecoin transparency is the distinction between claims and verification.

Attestations provide independent confirmation that reserves correspond to reported balances at a specific point in time. While attestations differ from full financial audits, they nevertheless represent an important layer of third-party validation.

The broader stablecoin market has increasingly moved toward this model.

Reserve reports, independent reviews, custody disclosures, and verification mechanisms are becoming standard expectations among institutional participants.

This trend reflects a growing recognition that trust is strengthened when information can be independently reviewed rather than simply asserted.

For corporate treasurers, the principle is straightforward: greater transparency generally enables more informed decision-making.

Why Reserve Structure Matters

Transparency is closely linked to reserve composition.

Stablecoins can be backed by different types of assets, including cash, short-term government securities, commodities, or combinations of multiple reserve instruments.

The reserve structure influences how users evaluate stability, liquidity, and risk.

This does not mean one reserve model is universally superior to another. Different structures are often designed for different objectives.

What matters is that reserve composition is clearly communicated and independently verifiable.

As institutional participation grows, market participants increasingly seek visibility into both the quality of reserves and the reporting standards surrounding them.

This trend extends across fiat-backed, commodity-backed, and real-world asset-backed digital assets.

Transparency Beyond Fiat-Backed Stablecoins

The transparency conversation is no longer limited to fiat-backed assets.

As tokenized real-world assets continue expanding, similar expectations are emerging across gold-backed stablecoins, tokenized commodities, and other collateralized digital assets.

Investors and institutions increasingly expect visibility into:

Reserve holdings.

Custody arrangements.

Verification processes.

Independent reviews.

Operational governance.

This reflects a broader maturation of digital finance where transparency becomes a core component of credibility.

The same principles that helped establish trust in certain fiat-backed stablecoins are increasingly influencing how other digital asset categories are evaluated.

How USDKG Fits Into the Transparency Conversation

USDKG approaches transparency through a different reserve model while operating within many of the same institutional expectations.

The stablecoin is issued by OJSC Virtual Asset Issuer, a state-owned entity operating under Kyrgyzstan's Ministry of Finance. Its initial issuance is backed by physical gold reserves independently audited by Kreston Global.

In addition, the project's smart contracts have undergone review by ConsenSys Diligence, providing independent verification of the underlying blockchain infrastructure.

The reserve model differs from fiat-backed stablecoins such as USDC, but the broader principle remains similar: transparency helps market participants understand how an asset is structured and what supports its value.

As the digital asset sector evolves, reserve verification and public disclosure are becoming increasingly important across a wide range of asset-backed models.

Institutional Adoption and the Importance of Trust

Institutional adoption is often discussed in terms of regulation, liquidity, and market access.

Trust is equally important.

For treasury teams, trust is typically built through clear reporting, independent verification, transparent governance, and predictable operational frameworks.

Stablecoins that provide visibility into these areas are often better positioned to support institutional evaluation processes.

This is one reason why transparency has become one of the defining themes across the broader stablecoin industry.

Whether reserves are backed by cash, government securities, physical commodities, or other assets, the ability to verify those reserves increasingly shapes how digital assets are perceived.

What Corporate Treasurers Can Take Away

The most important lesson from USDC's transparency model is not tied to a specific reserve structure.

It is the principle that trust becomes stronger when information is accessible, verifiable, and consistently communicated.

As stablecoins continue expanding into payments, treasury operations, settlement systems, and cross-border finance, transparency is likely to remain one of the most important factors influencing adoption.

Corporate treasurers evaluating digital assets are increasingly looking beyond market capitalization and focusing on the underlying frameworks that support credibility.

Reserve reporting, attestations, governance standards, and independent verification all contribute to this broader picture.

Conclusion

USDC helped establish transparency as a central component of institutional stablecoin adoption.

Its emphasis on reserve reporting, attestations, and disclosure has influenced how many organizations evaluate digital assets today.

As the market continues to mature, these expectations are extending far beyond fiat-backed stablecoins and into a growing range of asset-backed digital assets.

For corporate treasurers, the lesson is clear: understanding reserve structure is important, but understanding how those reserves are verified may be even more valuable.

Related Articles

July 14, 2026

The Stablecoin Market Is Entering Its Regulatory Era

Stablecoins are entering a new phase of development where regulatory clarity is becoming as important as liquidity and network effects. Around the world, jurisdictions are reshaping digital finance, making governance, transparency, and legal certainty increasingly central to long-term adoption.

June 30, 2026

Beyond Backing: What Tether’s aUSDT Closure Reveals About Commodity-Backed Digital Assets

The closure of Tether's aUSDT highlights a broader shift within the commodity-backed digital asset market. As adoption matures, utility, transparency, liquidity, and integration into financial infrastructure are becoming just as important as the assets held in reserve.

June 23, 2026

The Rise of Commodity-Backed Digital Assets in Global Finance

Commodity-backed digital assets are bringing tangible value into blockchain-based financial systems. As institutions place greater emphasis on collateral quality, transparency, and reserve integrity, assets such as gold, energy resources, and other commodities are becoming increasingly relevant within digital finance.